Greetings to all and happy July! I hope everyone enjoyed their Independence Day and watched some fireworks.

In order of our Country’s month of independence, I am going to quote the great Benjamin Franklin;

We all know that paying taxes is a part of life and it’s definitely a part of being an investor. To close out my estate planning series I wanted to cover a small item in the investment tax world; Cost Basis and the Step-Up in Cost Basis.

What is cost basis? Cost basis is the original value of an investment (what you paid for it). The difference between the value you purchased the investment (the basis) and the price you sold it for determines whether you have a gain or a loss in that investment.

For example:

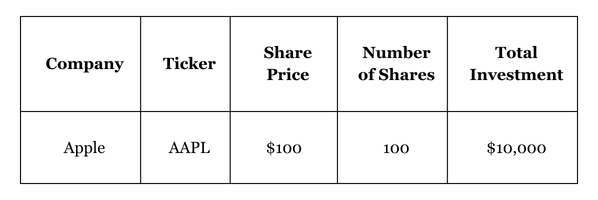

Let’s say Joe Blow the investor buys 100 shares of Apple stock (AAPL) today at $100 per share.

Joe’s basis is $100/share and $10,000 for the 100-share lot.

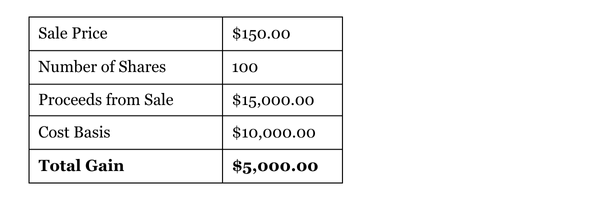

One year later, the stock has risen to $150/share. Joe decides to sell all 100 shares.

The amount received above the cost basis is considered a capital gain and is subject to capital gains tax. This is a normal part of investing and something that all investors deal with year over year. If we are paying taxes on our investments, that means the investments have performed well. While this is not the purpose of today’s article, it’s worth mentioning because it can be a source of frustration for the average investor. We never want to let the ‘tax tail wag the investment dog’ and so we make educated and intelligent investment decisions with the capital gains implications in mind. We don’t want to hold an investment simply to avoid paying taxes if there is a better way to deploy the money.

Let’s go back to Ben Franklin’s quote from earlier, “Nothing is certain except death and taxes.” As far as your investments go, this is mostly true but it does not take into account The Cost Basis Step-Up.

When an investor passes away, their assets are passed on to a named beneficiary either with a beneficiary designation, a trust, or a will. During that process, there can be an opportunity to exercise a step-up in the deceased investor’s cost basis. A step-up in basis will reset the purchase price of the investment to the value on the date of the original owner's death.

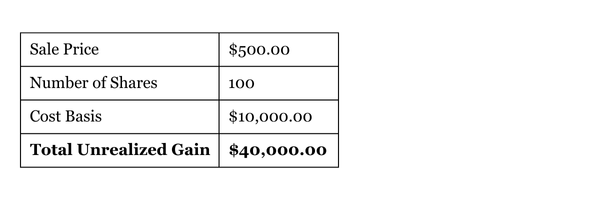

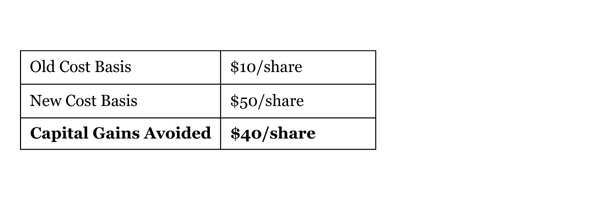

Let’s go back to the prior example. Let’s say Joe invested the $10,000 in Apple stock and it grew to $15,000. Instead of selling the stock he held onto it for another 10 years and the share price rose to $500/share now making his investment worth $50,000. If Joe sold the stock, he would realize a gain of $40,000 ($50,000 sale - $10,000 Cost Basis). Because the stock has not been sold, the gain is what we refer to as “unrealized” meaning that it has not triggered a taxable event. The gain is yet to be officially realized (you only realize a gain when you close out the investment by liquidating).

Joe passes away just shy of his 99th birthday. When the estate is settled the beneficiaries can realize a “Step-Up in Cost Basis” moving the Cost Basis from $10/share to the current share price of $50/share. His beneficiary can now sell the stock for a $0 gain.

Now let’s multiply this situation over a portfolio with a value of $1,000,000 or more. It’s not uncommon for accounts to have unrealized gains in the hundreds of thousands or millions of dollars. As investors age, it’s important that these types of tax-advantageous strategies are considered. With proper planning, we can effectively manage the portfolio for income and stay diversified without having to liquidate some of the more tax-sensitive investments. This gives the client the opportunity to pass some of their higher-performing investments to their heirs without having to ever realize the gain.

This is something that all investors should be aware of as part of their estate planning process.

It’s important to note that not all account types are entitled to a step-up in basis. Your specific portfolio and situation may determine a different course of action so it’s important that you understand your options and seek the advice of a qualified tax professional before making any changes.

If you would like to discuss your portfolio and your situation in more detail, please reach out to our team. A little planning can go a long way.

Important Disclosures:

Platte River Private Wealth and LPL Financial do not provide legal advice or services. Please consult your legal advisor regarding your specific situation.

Individual tax and legal matters should be discussed with your tax or legal professional.

LPL Financial representatives offer access to Trust Services through The Private Trust Company N.A. an affiliate of LPL Financial. (154-LPL)

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. All performance referenced is historical and is no guarantee of future results.

Any company names noted herein are for educational purposes only and not an indication of trading intent or a solicitation of their products or services. LPL Financial doesn’t provide research on individual equities.

Securities and advisory services offered through LPL Financial, a registered investment advisor. Member FINRA/SIPC. (finra.org, sipc.org)

The information contained in this e-mail message is being transmitted to and is intended for the use of only the individual(s) to whom it is addressed. If the reader of this message is not the intended recipient, you are hereby advised that any dissemination, distribution or copying of this message is strictly prohibited. If you have received this message in error, please immediately delete.

The LPL Financial registered representatives associated with this email may discuss and/or transact business only with residents of the states in which they are properly registered or licensed. No offers may be made or accepted from any resident of any other state.